IR-001 The Clean Path

IQD revalues. USD holds. You receive a windfall. Do you know what your government does to it the second it lands? Five countries. Five tax outcomes. One playbook.

This is the simplest version. IQD revalues. USD holds. You receive a windfall. What happens next?

Not "when." Not "how much." Those are the wrong questions right now.

The right question is: do you know what your own government does to that windfall the second it lands?

Because most people don't. And by the time they're Googling it, they've already made mistakes that cost them five or six figures.

This is what I'm personally researching. Not advice. Sourced data from government publications, central bank records, and tax legislation you can verify yourself. Every link is at the bottom.

What the CBI actually says

Let's start with what Iraq's central bank has publicly stated.

The official rate is 1,300 IQD to 1 USD. It's been anchored there since February 2023. The 2026 federal budget is drafted at that rate. Governor Ali Mohsen Al-Alaq has said there are "no plans to change the exchange rate."

The CBI is also working on a project to remove three zeros from the currency. That's a redenomination. Not a revaluation. The numbers get smaller. The purchasing power stays the same.

Clear enough.

Now here's what the same central bank is doing while saying all that.

They ended the dollar auction. Built a multi-currency direct banking platform that processes euros, dirhams, yuan, and Jordanian dinars. Restricted entire banks from touching USD. Rolled out ASYCUDA customs automation across every major port. Embedded US Treasury officials inside the CBI building itself.

And the country is spending $17 billion on a trade corridor that connects the Gulf to Europe through Iraq.

You don't build a $17 billion trade corridor at a program rate.

When a central bank says one thing and builds the opposite, you stop listening to the words and start watching the infrastructure.

The gap nobody talks about

Iraq's PM advisor publicly stated the country sits on more than $16 trillion in natural resources. Fifth-largest proven oil reserves. Second-largest phosphate reserves on earth. 10 billion tonnes. First globally in free sedimentary sulphur.

The GDP is $265 billion. The exchange rate values the economy at a fraction of what's in the ground.

Resource-to-GDP ratio: 60 to 1.

Saudi Arabia's ratio is 15 to 1.

Iraq has four times the resource gap of Saudi Arabia. At a program rate set during reconstruction. Twenty-two years ago.

The people who say "it's a scam" Googled it for five minutes. The people who say "it's real" spent 500 hours reading CBI publications and IMF Article IV reports.

Here's what the IMF actually found.

IMF Article IV. What the numbers say

The IMF's 2025 review of Iraq found:

- GDP contracted 2.3% in 2024. Oil production cuts.

- Non-oil GDP growth slowed to 2.5%, down from 13.8% in 2023.

- Budget breakeven oil price: $92 per barrel. One of the highest in OPEC.

- Fiscal deficit widened from 1.1% to 4.2% of GDP.

- Inflation dropped to 2.7%.

What does that tell you?

Iraq can't sustain itself at this rate. The budget breaks unless oil stays above $92. The IMF is projecting a 22% decline in oil prices. The math doesn't work at 1,300.

But the HCL is closer than it's ever been. Baghdad-Erbil signed a 10-point oil export agreement in August 2025. Maliki's 17-year veto is gone. The courts cleared the path.

Revenue sharing is the prerequisite. Always has been. The infrastructure is built. The compliance is built. The veto is removed.

What your government takes

This is the part nobody else in this space is covering. Because it's not exciting. It's not hopium. It's the difference between keeping your windfall and handing a third of it to your tax authority because you didn't know the rules.

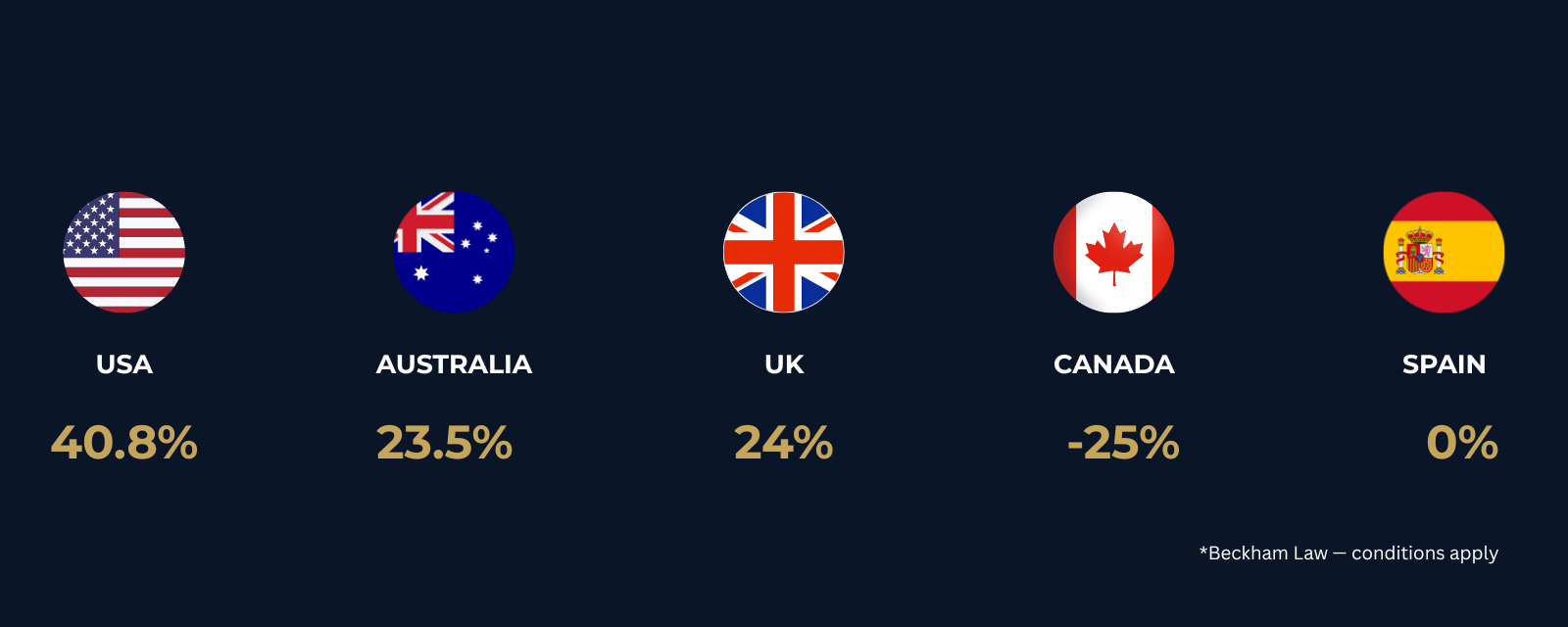

Here's how five countries treat a foreign currency gain right now.

March 2026. Current law.

United States

Foreign currency gains fall under Section 988 of the Internal Revenue Code. They're taxed as ordinary income. Not capital gains. Ordinary income. That means your marginal rate. Up to 37% federal, plus state, plus the 3.8% Net Investment Income Tax if you're above $200K.

Combined effective rate: up to 40.8%.

There's a $200 personal transaction exemption under Section 988(e)(2). But it applies per transaction, and only to "personal transactions." Speculative currency holdings almost certainly don't qualify.

The estate exemption was permanently set at $15 million per person under the OBBBA, signed July 4, 2025. $30 million for couples. Indexed for inflation from 2027.

Annual gift exclusion: $19,000 per recipient in 2026.

Australia

The ATO treats foreign currency as a CGT asset under Division 775 of the ITAA 1997. If you've held it for 12 months or more and you're classified as an investor (not a trader), you get the 50% CGT discount.

Effective rate with the discount: roughly 23.5% at the top marginal rate.

No de minimis exemption. Australia doesn't have the US $200 rule. Every dollar counts.

United Kingdom

HMRC treats foreign currency as a chargeable asset for CGT. Computed in GBP.

There's a personal expenditure exemption under CG78315. But it only covers currency acquired for personal spending abroad. Investment holdings don't qualify.

Annual CGT exempt amount: GBP 3,000. That's it. Three thousand pounds. For the year.

Rates: 18% basic rate, 24% higher rate. Changed October 30, 2024.

Canada

CRA treats forex dispositions as capital gains under ITA subsection 39(2).

There's a $200 CAD de minimis. But that's on your annual net gain or loss, not per transaction.

Capital gains inclusion rate: 50%. The proposed increase to 66.7% was cancelled on March 21, 2025. The 50% rate is permanent.

Spain

If you qualify for Spain's Beckham Law, and currency holders relocating to Spain potentially can, foreign-source capital gains are completely exempt from Spanish tax. Zero.

The regime lasts 6 years. Flat 24% on Spanish-source employment income up to EUR 600,000. Everything earned or gained outside Spain: not taxed.

Eligibility requires an employment trigger. A job, a Digital Nomad Visa, or a director position in a Spanish company. Freelancers generally don't qualify. The non-residency requirement was reduced from 10 to 5 years in 2023.

If you don't qualify for Beckham, the standard savings scale runs 19% to 30%. Plus wealth tax. Plus the Modelo 720 foreign asset reporting requirement.

The difference between qualifying and not qualifying could be hundreds of thousands on a large gain.

What happens at the bank

Iraq is not on the FATF grey list or black list. It was removed from monitoring in June 2018. The compliance is not the issue.

The issue is your receiving bank.

Any incoming wire over $10,000 triggers a Currency Transaction Report to FinCEN. That threshold hasn't changed since 1970. In today's money, that's roughly $80,000. Every large transaction files automatically.

If the wire originates from Iraq, your bank's compliance team will request source-of-funds documentation. Proof of purchase. Proof of identity. Proof of where the currency came from and how it was exchanged.

This is standard AML procedure. It's not a red flag. But if you don't have your paperwork ready, your funds sit in limbo while the compliance team reviews. That can take weeks.

Something else to watch.

The CBI has been restricting Iraqi banks from handling USD transactions. Entire banks cut off. The list was published February 23, 2026. Fewer Iraqi banks can originate compliant USD wires. That's fewer clean pipes for large transfers.

And while traditional banks are tightening the transaction side, they're doing something else.

JPMorgan tripled its Private Client locations in September 2025. Expanded to 53 Chase branches. Opened 14 new Financial Centers across four states, specifically targeting affluent clients. Plans to open 160+ more in 2026. These aren't transaction branches. They're wealth advisory centres.

Wells Fargo called 2025 its "best recruiting year in a decade." All three advisory channels added more advisors than they lost. They recruited a $3.1 billion team from JPMorgan, a $3 billion team from Merrill Lynch, a $1.2 billion team from Citi.

Goldman Sachs is growing its wealth management division faster than its banking division. The CEO said publicly he wants to "put more feet on the ground."

Thrivent hired 600 financial advisors in 2026 alone.

McKinsey projects 110,000 financial advisors will retire by 2034. The industry calls it the "Great Wealth Transfer." $124 trillion moving between generations by 2048.

The banks say they're building for inheritance. Maybe they are. But when 89% of high-net-worth firms make wealth services their number one growth strategy in the same 12-month window, you stop listening to the explanation and start watching what they build.

The windfall playbook

Fidelity, UBS, FINRA, and Baird all say the same thing. The worst financial decisions are made in the first 48 hours after sudden wealth.

Phase 1. Pause. Zero to six months. Park the funds in Treasuries or a high-yield savings account. Process what just happened. Don't buy anything. Don't lend anything. Don't tell anyone who doesn't need to know.

Phase 2. Assemble your team. CPA first. Immediately. Before you spend a dollar. Estate attorney. Fee-only fiduciary financial advisor. Not commission-based. Fee-only. They work for you, not for the product they're selling.

Phase 3. Protect. Umbrella insurance. Estate plan update. The $15 million exemption under OBBBA is generous, but 40% estate tax kicks in above that. Trusts may be appropriate depending on your situation. That's between you and your attorney.

Phase 4. Deploy. Dollar-cost average into the market over 6 to 12 months. Diversify across asset classes. Tax-efficient placement. Don't chase what's already moved.

Phase 5. Maintain. Quarterly estimated tax payments so the IRS doesn't hit you with underpayment penalties. Regular rebalancing. Review every 6 months with your advisor.

None of this is advice. This is what every major wealth manager publishes openly. The question is whether you've read it before you need it.

One more thing. The playbook above is what the industry tells you. There are trust structures that most financial advisors won't mention. Not because they're illegal. Because the advisor's compensation model doesn't reward them for moving your assets out of their management. Irrevocable trusts. Domestic asset protection trusts. Structures where the timing of setup, before vs after a windfall, changes the tax outcome by six or seven figures.

That's a full report on its own. It's coming.

What's next

This is the clean path. One currency moves. Your home currency holds. The question is tax treatment and capital deployment.

It's also the simplest version of what could happen. And probably the least likely to play out exactly this way.

What if the dollar is losing purchasing power while you hold your windfall? It's dropped 24% since 2020. Gold is up 54% in 12 months. The DXY fell 10% in 2025 alone.

What if multiple currencies move at once? The exchange infrastructure doesn't exist for all of them in one place. There's no single bank or platform that handles IQD, VND, and others simultaneously.

What if the banking system itself isn't stable when you try to access your capital? Cyprus confiscated 47.5% of deposits over EUR 100,000 in 2013. Capital controls lasted two years. People couldn't withdraw more than EUR 300 a day.

And what if this takes another 18 months? Gold costs more every month you wait. Property in dollarised economies like El Salvador and Panama is genuinely appreciating. Not currency devaluation. Real price increases. Visa thresholds are rising or disappearing. Spain's golden visa is already gone. Greece doubled its minimum. The window is closing while you wait.

Each of those requires different preparation. Different research. Different positioning.

The full series is available to Intelligence Subscribers.

The Intelligence Report Series

This report is one of six. Each covers a different scenario and what it means for your positioning. The clean path is the simplest. The others get harder.

IR-001 The Clean Path - You just read it. One currency moves. Yours holds. Tax treatment and deployment.

IR-002 The Long Wait - What every month of delay costs you. Gold, property, visa windows. The price of inaction.

IR-003 The Dollar Erosion - Your measuring stick is not stable. What happens when the currency you convert into is losing value at the same time.

IR-004 The Structures They Won't Mention - Trust structures, asset protection, and the timing decisions that change outcomes by six figures.

IR-005 The Handover - How the banking system is being re-functionalized from deposit-taker to wealth office. The documented transition under GENIUS Act, Trump Accounts, Gold Card, and Basel III endgame.

IR-006 The Multi-Currency Event - When multiple currencies move at once. Infrastructure gaps, exchange logistics, and multi-jurisdiction positioning.

Sources

All data in this report sourced from government primary publications and official secondary sources. Verify everything yourself.

CBI / Iraq:

- CBI Exchange Rate Series

- Iraq Business News -- Banks Restricted from USD

- IMF 2025 Article IV

- EIA Iraq Country Analysis

- Iraq PM Advisor -- $16T Resources

- FATF -- Iraq

Tax:

- 26 USC Section 988

- IRS Practice Unit -- Foreign Currency

- OBBBA Estate Exemption

- ATO -- CGT and Forex

- HMRC CG78315

- CRA Capital Gains 2025

- FinCEN -- CTR Guide

Banking Signals:

- JPMorgan Private Client Expansion

- JPMorgan 14 New Financial Centers

- Chase 160+ Branches 2026

- McKinsey -- Looming Advisor Shortage

- Cerulli -- $124T Wealth Transfer

- Thrivent Hiring 600 Advisors

Windfall Management:

Not financial advice. Sourced research for informational purposes only. Consult a qualified professional in your jurisdiction before making any financial decisions.